Mumbai: Minister of Finance and Corporate Affairs Smt. Nirmala Sitharaman today unveiled the fourth edition of the Public Sector Bank (PSB) Reforms Agenda ‘EASE 4.0’ for 2021-22 – tech-enabled, simplified, and collaborative banking. She unveiled the annual report for the PSB Reforms Agenda EASE 3.0 for 2020-21 and participated in the awards ceremony to felicitate best performing banks on EASE 3.0 Banking Reforms Index.

Shri Pankaj Jain, Additional Secretary, Department of Financial Services, Shri Amit Agrawal, Additional Secretary, Department of Financial Services & Chairman IBA, Shri Rajkiran Rai G., were also present at the event.

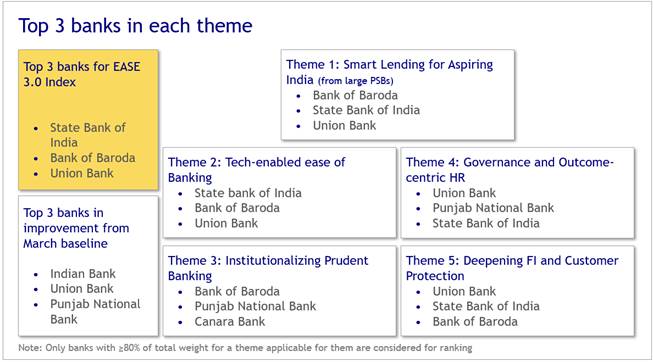

SBI, BoB, Union Bank of India win the top awards for PSB Reforms EASE 3.0

SBI, BoB, Union Bank of India won the awards for best performing banks for PSB Reforms EASE 3.0 based on the EASE index. Indian Bank won the award for the best improvement from the baseline performance. SBI, BoB, Union Bank of India, PNB, Canara Bank won the top awards in different themes of the PSB Reforms Agenda EASE 3.0.

EASE program is driven by IBA and BCG is the knowledge partner for the EASE program for the fourth year running.

Overall performance

- PSBs have reported a profit of INR 31,817 crore in FY21 as compared to a loss of INR 26,016 crore in FY20. This is the first year when PSBs have reported profit after five years of losses.

- Total gross non-performing assets stood at INR 6.16 lakh crore as of March 2021, reduction of INR 62,000 crore from March 2020 levels.

- Number frauds at PSBs have substantially come down to 2,903 in FY2020-21 compared to 3,704 in FY2018-19

Digital Lending

- Credit@click was a flagship initiative under EASE 3.0. Top 7 PSBs (based on total business size as of 1st April 2020) have set up mechanisms for instantaneous and contactless access to credit through end-to-end digitalisation of key retail and MSME credit products. For unsecured personal loans (UPL), INR 5,502 crore of fresh loans and for small credit loans, INR 124 crore of fresh loans were disbursed end-to-end digitally in quarter ended March 2021 (2X growth in unsecured personal loans and 10X growth in small credit loans compared to quarter ended March 2020). Nearly 4.4 lakh customers have been benefitted through such instantaneous and simplified credit access.

- PSBs have setup mechanism for customers where they can register loan requests 24X7 through digital channels such as Mobile and Internet banking, SMS, missed call and call centre. In FY21, PSBs have collectively disbursed INR 40,819 crore of fresh personal, home and vehicle loans through leads sourced from such digital channels. This accounts for approximately 10% of overall disbursements in personal, home and vehicle loans in the above said period.

- The top 7 PSBs have built analytics capabilities through the setup of dedicated analytics teams and IT infrastructure to proactively offer loans to its existing customers. Such loan offers were generated using the existing customer transactions data within the banks. In FY21, INR 49,777 crore of fresh retail loan disbursements were made by the top 7 PSBs based on these credit offers.

- PSBs have also extensively used external partnerships and dedicated marketing salesforce network for the sourcing of retail segment and MSME segment loans. Sourcing from such channels has been 9.1 lakh loans in FY21.

Mobile/Internet Banking and Customer Service

- The base of PSB customers which are active on mobile and internet banking channels has increased from 3.4 crore in quarter ended March 2021 to 7.6 crore in quarter ended March 2021. Nearly 72% of financial transactions happening at PSBs in now happening through digital channels.

- PSBs are now offering services across call centres, Internet banking, and Mobile banking in 14 regional languages such as Telugu, Marathi, Kannada, Tamil, Malayalam, Gujarati, Bengali, Odia, Kashmiri, Konkani, Hindi, Punjabi, Assamese for the ease of customers.

- 96% of PSB branches now have at least one officer fluent in conversing in local languages in Q4FY21.

- For continual improvement in coverage under financial inclusion initiatives, there was a 13% growth in transactions provided by Bank Mitras in rural areas and 50% growth in enrolments in Micro personal accident insurance in Q4FY21 compared to Q4FY20.

Credit Risk and Prudent Banking

- PSBs have adopted digital platforms such as online OTS, e-Bक्रय, e-DRT for expedited recovery. Nearly ~INR 4,068 crore value of assets recovered via e-listing on e-Bkray platform in FY21.

- With the deployment IT-based Early Warning Signals (EWS) systems nearly complete by all PSBs in EASE 2.0, coverage under EWS has also increased significantly. INR 33 lakh crores loan book covered under EWS at the end of March 2021.

Like in the previous years, progress made by PSBs was tracked quarterly through a published EASE Reforms Index leading up to the annual review. The Index measures the performance of each PSB on 135+ objective metrics across five themes. It provides all PSBs a comparative evaluation showing where banks stand vis-à-vis benchmarks and peers on the Reforms Agenda. The Index follows a fully transparent scoring methodology, which enables banks to identify precisely their strengths as well as areas for improvement. The goal is to continue driving change by spurring healthy competition among PSBs and also by encouraging them to learn from each other.

The transformational measures have helped convert many of these Banks into financially resilient, self-sustaining entities that are now competing aggressively in the marketplace.

Performance of PSB on EASE 3.0 Index

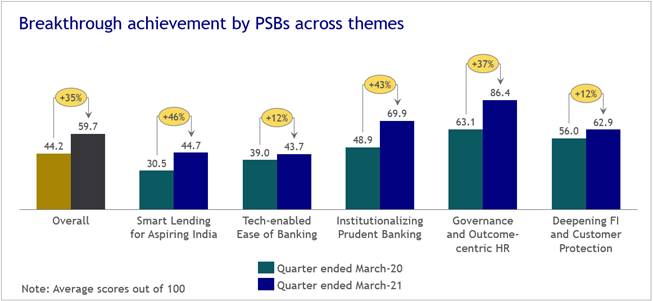

PSBs have recorded a phenomenal growth in their performance over four quarters since the launch of EASE 3.0 Reforms Agenda. The overall score of PSBs increased by 35% between March-2020 and March-2021, with the average EASE index score improving from 44.2 to

59.7 out of 100. Significant progress is seen across six themes of the Reforms Agenda, with the highest improvement seen in the themes of ‘Smart Lending’ and ‘Institutionalising Prudent Banking’.

EASE 4.0 Reforms Agenda commits Public Sector Banks to Tech-Enabled Banking, simplified and collaborative banking

A common reform agenda for PSBs, EASE Agenda is aimed at institutionalizing clean and smart banking. It was launched in January 2018, and the subsequent edition of the program ― EASE 2.0 built on the foundation laid in EASE 1.0 and furthered the progress on reforms. EASE 3.0 was launched in for FY2020-21.

EASE has become the cornerstone of reforms in PSBs. The institution of the comprehensive index has catalysed accelerated implementation of several initiatives and has injected greater customer-centricity in PSBs’ business model and processes. PSBs have fundamentally re-oriented their ways of working to align with EASE methodology and have made concerted efforts to deep-root reforms and maximise the value derived from them.

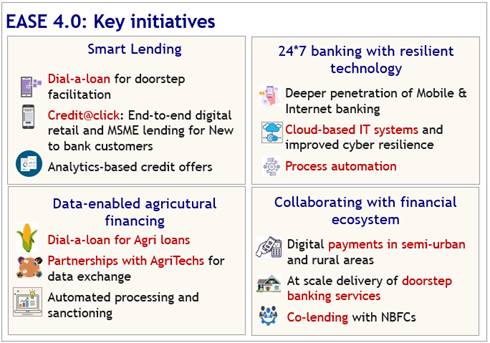

The next edition of EASE reforms i.e. EASE 4.0 aims to further the agenda of customer-centric digital transformation and deeply embed digital and data into PSBs’ ways of working.

Under EASE 4.0, PSBs to offer:

- New Age 24×7 banking with resilient technology to deliver uninterrupted banking services by strengthening technology systems and internal processes in the PSBs to delivery such services

- Digital and data-enabled Agri financing through measures such as Agri loan initiation via digital channels such as SMS, missed call, call centre, Internet and Mobile Banking, etc., partnerships with third parties and AgriTechs for alternate data exchange, end to end digitized processing and sanction of agricultural loans

- Improved access to doorstep banking services launched by PSBs by promoting awareness and encouraging usage of such services and time-bound actions for service delivery

- Promoting digital payments in semi-urban and rural areas through adoption of NFC, Bharat QR-based payment solutions, etc. to increase the use of digital modes of payment

- Proactive analytics-based credit and non-credit product out-reach to retail and MSME customers

- Deeper penetration of Mobile and Internet Banking services including availability in regional languages

- Collaborative banking for synergistic outcomes through collaboration between PSBs and with broader financial services ecosystem such as NBFCs for the coordinated handling of co-originated loans

- Increasing time spent on strategy and planning related discussions by Board

PSBs have already started taking steps based on the reforms agenda. During the event, PSBs shared many thoughts on how these reforms have benefitted them and the new initiatives underway in their respective banks. Progress of PSBs will continue to be tracked on metrics linked to Reform Action Points, and their progress will be published through a quarterly index.

PSBs have stepped up to support the country during COVID-19

Despite the COVID-19 crisis, Public sector banks continue to provide uninterrupted service and credit delivery to its customers. They have also been at the forefront of extending banking services in the remotest parts of the country.

From different modes of staffing to remote working, 80,000+ bank branches were operational during COVID-19. Additionally, there has been around two times increase in Aadhaar Enabled Payment System (AEPS) transactions through micro ATMs, and enhanced doorstep banking support by 75,000+ Bank Mitras. To further support the customers in these times, the banks have drastically increased the number of services being offered at the call centers, to 23 as of March-21 in 13 regional languages. More than 42 crore people received financial assistance of Rs 68,820 crore under the Pradhan Mantri Garib Kalyan Package till September 2020.

{kind=link}

Discussion about this post